Jahez needed Snoonu

Snoonu arrived at an important time for Jahez as pressure in Saudi continues to build.

A quick sidenote before today’s piece.

For many of my writings on Termsheet, I regularly research public companies in the Middle East and have realized that public market data in the region is surprisingly difficult to work with.

You sometimes end up with 10 browser tabs open just to understand basic things about a single company.

To solve this, I recently started building this little thing called Premargin.

It tracks listed companies across Saudi Arabia, UAE, Qatar, and Kuwait with their financials, disclosures, and fundamentals in one place.

Pretty lightweight right now, but useful. I use it myself for a lot of the research behind these pieces.

But I need help figuring out what we should add and improve before rolling new stuff out.

If you work with public equities in the region in any capacity, I’d love to speak with you and understand how Premargin can become more useful. Just reply to this email and I’ll get in touch.

Now to today’s piece.

When Jahez acquired Snoonu last year, the deal valued Snoonu at more than one-fifth of Jahez’s own market capitalization at the time.

At the time, the deal looked expensive to many from the outside.

But delivery acquisitions in the Middle East have a long history of looking expensive initially and later turning out to be strategically important for the buyer.

Talabat. HungerStation. Carriage. InstaShop. Zomato UAE. Even Turkey’s Yemeksepeti.

Most looked expensive in the moment. Many aged very well.

Jahez announced the acquisition of 76.5 percent of Snoonu in July 2025 for $245 million.

At the time, Jahez itself was trading at a market cap of around $1.5 billion.

That means Jahez paid an amount equal to roughly 16 percent of its market cap, or about 21 percent on an implied valuation basis.

And this was not a small company.

Snoonu was generating around $140 million in annual net revenue and growing significantly faster than Jahez itself.

For comparison, Jahez was doing a little over $590 million in net revenue at the time. Snoonu would have represented roughly 19 percent of the combined entity’s revenue base.

(Strategic acquisitions are rarely judged on near-term revenue contribution alone. Salesforce, for example, paid an amount equivalent to roughly 12 percent of its own market value for Slack despite Slack contributing less than 5 percent of combined revenue at the time).

On 2024 numbers, Jahez paid around 2.3x Snoonu’s revenue while Jahez itself traded at around 2.5x revenue.

On earnings, the multiple looked more expensive. But strategically, the acquisition already looked reasonable based on growth and scale alone.

The more important thing however was timing.

Jahez announced the acquisition almost three quarters after Keeta entered Saudi Arabia.

By then, the company had likely seen enough to realize that growth in Saudi was going to become increasingly difficult as long as Keeta continued funding all sides of the marketplace with subsidies.

And that should have played a major role in the decision to acquire Snoonu.

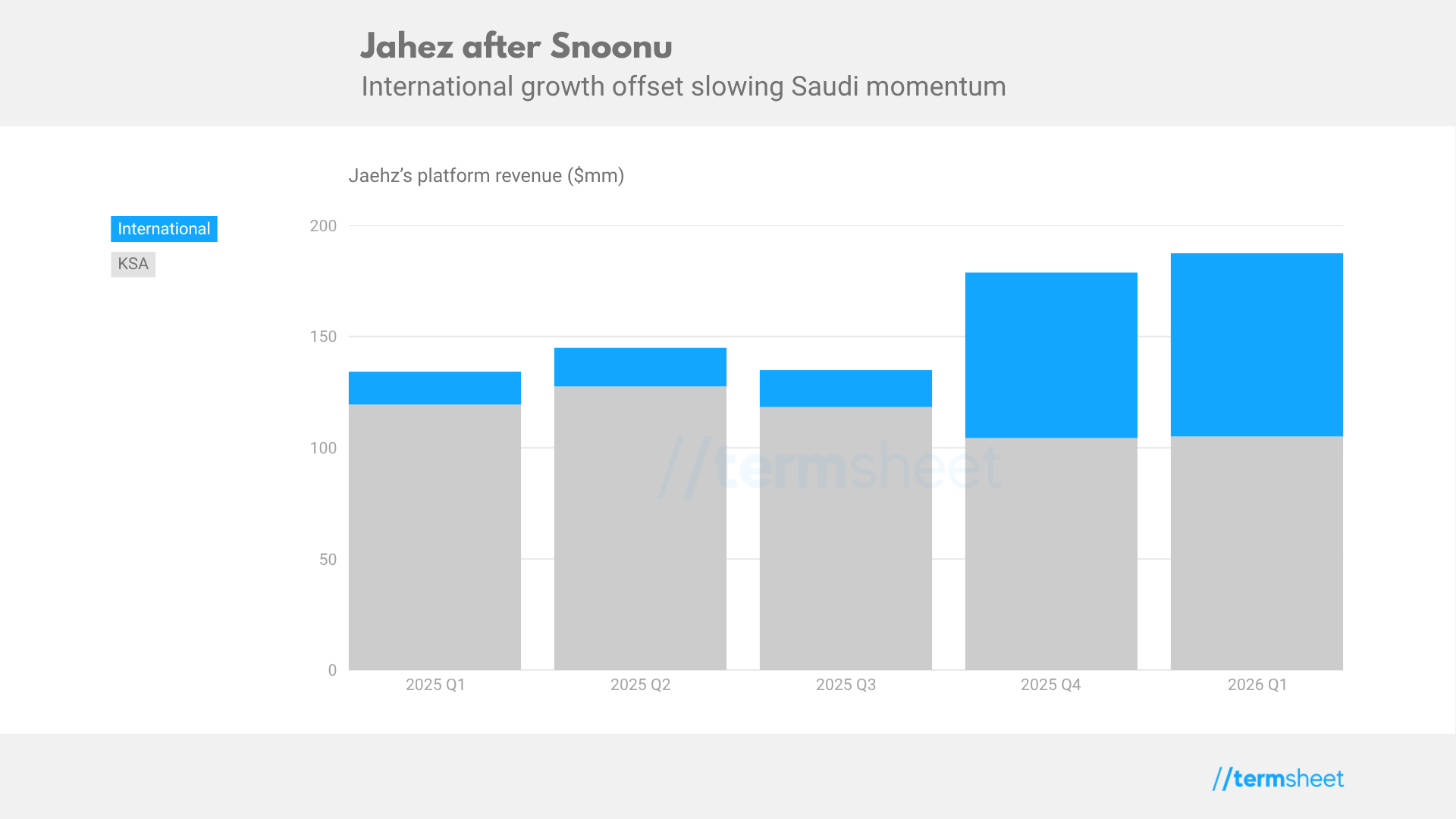

The latest earnings now show how important Snoonu has become inside the Jahez universe.

The company noted in its Q1 2026 earnings:

“Group net revenue grew 37.9% YoY to SAR 725.1 million [$193.2 million], driven primarily by the consolidation of Snoonu, which led to a 5.6x revenue growth in Jahez’s non-KSA segment, more than offsetting a 12.0% decline in the KSA segment.”

Based on Termsheet estimates, Snoonu’s contribution to Jahez’s Q1 2026 revenue was likely between $60 million and $70 million.

That would mean Snoonu potentially contributed up to 36 percent of Jahez’s total quarterly net revenue.

In other words, without Snoonu, Jahez’s group revenue in Q1 2026 would likely have declined by over 5 percent.

The shift becomes much clearer when looking at Jahez’s revenue mix over the last year.

Before Snoonu consolidation in Q4 2025, as the chart highlights, international operations represented a relatively small part of the business. Within a quarter, they became a major contributor to overall revenue growth as Saudi momentum slowed.

That still hasn’t stopped Jahez’s stock from getting crushed, though.

Since the acquisition, the company’s market cap has fallen more than 55 percent and currently stands at around $682 million.

So despite the company making significant progress in rest of the region through Snoonu, Keeta’s aggressive expansion in Saudi continues to weigh heavily on investor sentiment.

But without Snoonu, the situation may have looked significantly worse.

With margins compressing and growth slowing in its core market, Jahez would have had little growth left (if any at all) to show at the group level.

One positive sign from the latest earnings however was management noting that the company expanded market share in Saudi during Q1 2026 versus Q4 2025, although it did not disclose the exact figures.

The market, however, remained unconvinced.

Jahez’s stock fell more than 7 percent on the day it announced earnings and is down more than 12 percent since then.

Investors appear far more focused on the pressure Keeta continues to create in Saudi.

Which is also what makes Snoonu increasingly important for Jahez.

The acquisition was initially framed as international expansion. Increasingly, it is also starting to look like a partial buffer against the pressure building in its core market.

Hi Zubair, can you consider adding a snapshot of the company’s background that is under discussion for the future? I had no idea what Jahez was and learnt through comparison with Keeta that we’re discussing delivery apps. A short background of the companies plus the deal in question would be very useful for a reader like me that can then be followed up with the discussion.